MUMBAI: The Reserve Bank of India’s move to curb the number of free transactions in automated teller machines (

MUMBAI: The Reserve Bank of India’s move to curb the number of free transactions in automated teller machines (A report by Ashish Das — a

The RBI had reduced the number of free transactions of third-party bank ATMs, effective November, following protests by banks that they were losing money because of their customers’ frequent cash withdrawals.

Today, a third of all cash withdrawals takes place at third-party ATMs. Average third-party ATM transaction volume had soared by 70% to 1,300 per month in 2010 after the RBI brought in the concept of free unlimited withdrawals at ATMs of other banks. However, the figure dropped to 1,150 after RBI capped monthly withdrawals at other banks’ ATMs at five.

The report estimates that the average transaction in an ATM costs banks less than Rs 17 even after factoring in the new security measures that they are required to install. But this is assuming that the number of transactions do not fall.

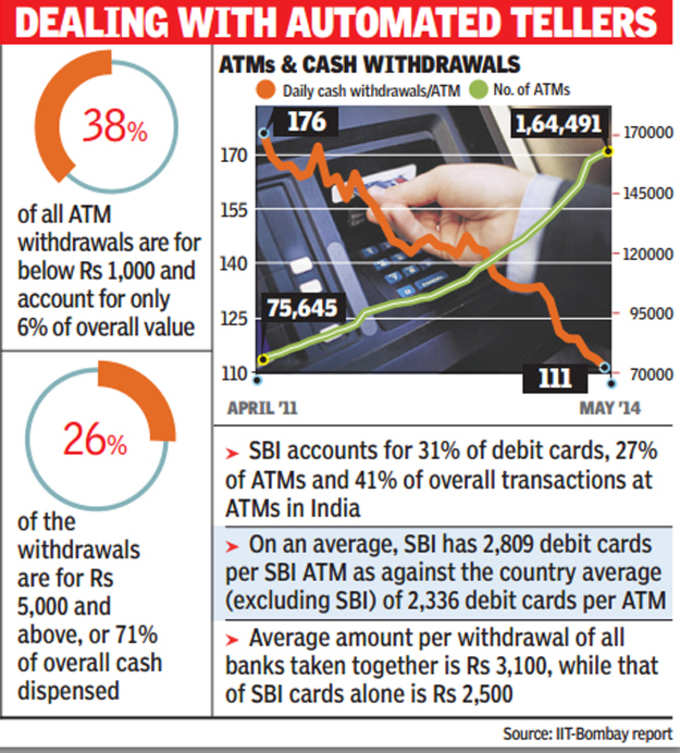

In the last three financial years, the number of ATMs grew at a sharp rate of 112%, but there has been a 35% reduction in the average number of financial transactions per ATM. The average number of withdrawals per day have dropped from 176 per day to 111 per day from April 2011 to May this year.

There is a risk that this number could fall further as banks are planning an even greater number of ATMs and private operators are in the process of installing thousands of ‘white label’ ATMs.

According to Das, in an ideal situation, use of each other’s ATMs is expected to more or less nullify the interchange charges that banks pay one another. But some banks end up being net payers because they have issued more cards in proportion to their ATMs. Banks like SBI are also hit because withdrawal by its own customers is low-value, whereas private bank customers make large, chunky withdrawals from SBI’s ATMs. But in both cases, the interchange fee is the same, irrespective of value.

The report recommends banks pay each other a fixed fee of Rs 5 plus 0.2% of the amount withdrawn, subject to a cap of Rs 25 per transaction. “The impact of bringing in behavioural changes in ATM usage through reducing cross-ATM usage (by imposing a fee) is not to the gain of banks and customers alike. It would invariably reduce the number of overall usage per ATM and thereby increase inefficiency and cost to banks to run ATMs even for their own customers. Furthermore, such a change will force an increase in cash-in-hand with bank customers as they will lean towards withdrawing more cash than required to avoid frequent ATM use and consequential fees,” the study said.