But, the only trouble is that these additional features have a hefty premium, say experts. So, many of them are asking individuals to go for basic policy first and then consider adding useful features to it if they have the resources.

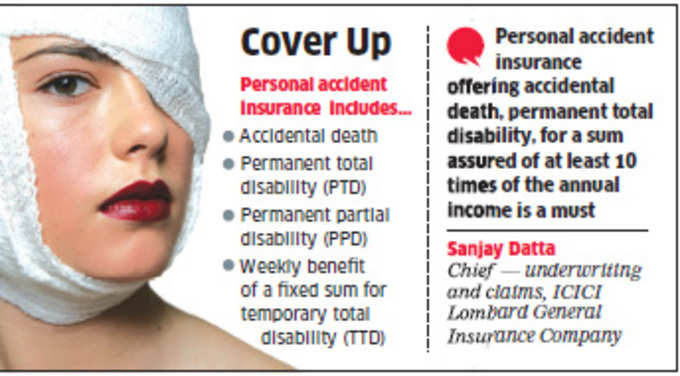

“Personal accident insurance offering accidental death, permanent total disability, for a sum assured of at least 10 times annual income is a must. Plans with more features can be bought if the budget permits and if an individual needs,” says Sanjay Datta, chief — underwriting and claims,

|

Though the bouquet of benefits looks good, each of these comes at a cost. For example, while the basic plan that offers accidental death, PTD and PPD benefit for a sum assured of Rs10 lakh can be secured at Rs1,100-1,200 per year, TTD benefits may cost almost 50% more than the basic plan. If more features such as accidental medical expenses benefit are added, you may have to pay 10% to 30% more. The final number keeps increasing as you keep adding the features to the basic plan.

While the cost should have a bearing on the buying decision, one should not altogether avoid extra features or high sum assured, say experts. “Your approach to buying personal accident insurance cover should be —first buy a basic cover; if you have money go for more features, and if your budget still permits, go for a high sum assured,” says Sudhir Sarnobat, CEO, medimanage.com, a health insurance advisory. For example, an individual with an annual income of Rs5 lakh should have a basic accident insurance plan for a sum assured of Rs50 lakh.

If he can afford to spend more, more features can be looked at. “While shopping for additional features, individuals must decide using two factors — what is the possibility of the insured meeting with a risk arising out of an accident and how much benefit would be paid by the insurance company,” adds Sarnobat. For example, a salaried individual working as an office staff, who has a ‘paid leave’ offered by his employer, may ignore buying TTD benefit.

He may not be in the high risk zone and can afford to stay at home for four weeks due to TTD arising out of an accident. Compare him with a self-employed professional, who may be travelling a lot and doesn’t have a ‘paid leave’, he should be buying a weekly benefit for TTD. “You have to look at each benefit in absolute terms, too. Some of these benefits may be irrelevant in some cases,” says an

For example, transportation of family benefit is useless if you do not have a family, or you always travel with your family. Also each of these add-on benefits has sub-limit. House or vehicle modification expense is capped at lower of Rs1 lakh or 10% of sum assured.