The fall of Yes Bank founder Rana Kapoor from a billion dollars to facing a ₹4300 crore investigation

Mar 9, 2020, 13:39 IST

- Kapoor was in the limelight due to the fast rise of its bank. Its stock shot up from ₹12.5 in June 2005 to ₹393.20 in August 2019.

- In just over 17 years, the bank became India’s fourth-largest private lender.

- However, the downfall of Yes Bank and Rana Kapoor came as fast as its rise.

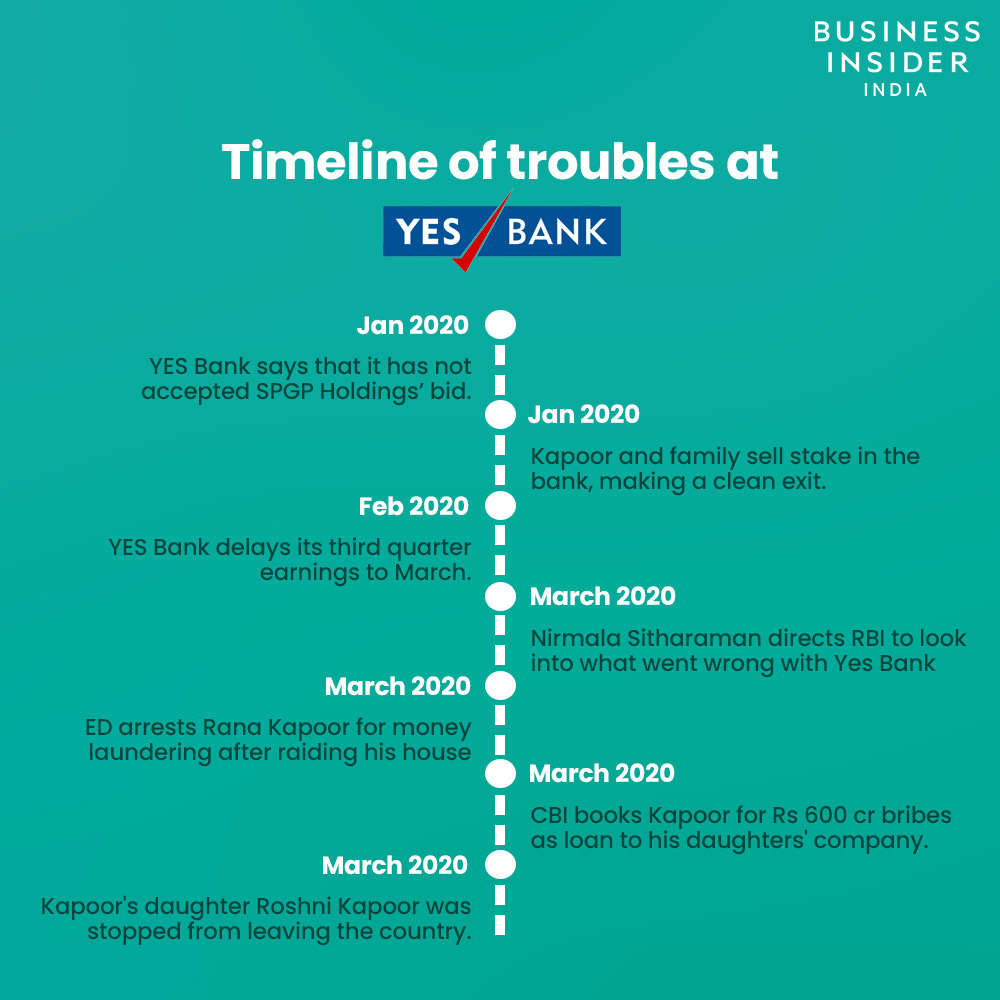

- Rana Kapoor was taken into custody by the Enforcement Directorate (ED) on charges of money laundering, allegedly worth ₹4,300 crore, during his tenure.

Advertisement

India’s second richest banker Rana Kapoor — former MD and CEO of troubled Yes Bank — was taken into custody by the Enforcement Directorate (ED) on charges of money laundering worth ₹4,300 crore, during his tenure. The 62-year old Kapoor co-founded Yes Bank alongside Ashok Kapur in 2004. In just over 17 years, the bank became India’s fourth-largest private lender. However, the downfall of Yes Bank and Rana Kapoor came as fast as its rise.

On March 5, the Reserve Bank of India (RBI) superseded Yes Bank’s board and imposed a withdrawal limit of ₹50,000 on its customers for a month. Like many other banks in India, Yes Bank was stressed under a load of bad loans. However, the Enforcement Directorate (ED) stepped against its probe on Kapoor due to the bank’s irregular credit practices leading to suspicions of money laundering and insider trading.

The rise of a billionaire promoter

Rana Kapoor started Yes Bank at a time when the country didn’t have many banking entrepreneurs. Uday Kotak was the only one leading the charge on private banking. And, Kapoor wanted to model Yes Bank after Kotak Mahindra Bank.

Advertisement

He infused ₹200 crore capital with his brother-in-law Ashok Kapur, who is now deceased. A year later, the bank raised ₹300 crore through an initial public offering (IPO). Soon after its debut, Yes Bank stock became the apple of investor’s eye and it looked like nothing could go wrong. But it was a rocky ride for Yes Bank. Three years after it went for an IPO, Kapur the then chairman of Yes Bank died in 2008 Mumbai terrorist attack. His wife Madhu Kapur later inherited his 12% stake after a nasty court battle.

Over the span of a decade, the bank recorded a 30% increase in its profit during the October-December quarter of 2016. ICICI Securities also recommended buying Yes Bank shares after it showed “strong business growth” in 2017.

The Good and the bad times

Kapoor was in the limelight due to the fast rise of its bank. Its stock shot up from ₹12.5 in June 2005 to ₹393.20 in August 2019.

In January 2019, he entered the billionaire club after his net worth surged. His 11.6% stake in the bank was now worth $1 billion, according to Bloomberg. For a while, it looked like Kapoor would achieve his dream as he became the second richest banker in India after Uday Kotak. He was looking to double Yes Bank’s market share from 1% to 2.5% in 2020.

Advertisement

But little did he know that growth itself would punch a hole in the bank. The bank came on RBI’s radar for its penchant for loaning to corporates that other banks wouldn’t entertain and quoting high-interest rates. While he did successfully recover a few loans like from the defunct Kingfisher Airlines owned by Vijay Mallya — his model was heading for failure, as the economy slowed down.When RBI ousted Rana Kapoor as the CEO

In 2016, RBI’s assessments discovered that Yes Bank was sweeping a lot under the carpet. It had under-reported non-performing assets (NPAs) worth ₹4,176 crore ($580 million) for March 2016. In 2017, the extent of underreporting swelled to ₹6,355 crore. As a result, its plan to raise $1 billion through qualified institutional placement failed terribly, leading it to the funding crisis that eventually led to its downfall.

Thanks to the many gimmicks, RBI also ousted Kapoor from the bank by trimming his tenure to January, 2019.

Advertisement

Soon, many secrets came tumbling out. Nearly ₹10,000 crore worth loans (about 4% of all its loans) given under Rana Kapoor’s management were classified as high-risk. In simple words, loans that may turn bad in a year.

In fact, Yes Bank had exposure to almost all the troubled groups and companies in the country — Jet Airways, Anil Dhirubhai Ambani Group, Cox & Kings, CG Power, Dewan Housing Finance (DHFL), Essar Shipping, Mcleod Russel, Cafe Coffee Day etc.

Troubled Times

Even after Yes Bank appointed Ravneet Gill as Rana Kapoor’s successor in March 2019, its troubles were far from over. It posted a shocking loss of ₹600 for the quarter ending September 2019. While the revenues fell 20%, costs rose through the roof shrinking operating profit by 40%.

Advertisement

Soon, there were a flurry of rating downgrades from Moody’s and others after news about NPA’s doubling to 9.5% of total loans in FY21, started doing the rounds. IDFC Securities cut the target price for the share price by more than half to ₹35. Yes Bank’s share slipped by 93% since its peak of August 2018.

Rana Kapoor to blame

Most industry experts are blaming Rana Kapoor and his non-traditional ways for the fall of Yes Bank — and crippling India’s banking sector even further. The ED and CBI now believe that the robust growth of Yes Bank was based on unethical and illegal practises. He is also being booked for accepting bribes in the form of loans to his daughters’ company.

However, Kapoor still maintains that he has “no clue” why the RBI took over the bank he built from scratch.

Advertisement

See also:

Yes Bank mobile and net banking down after RBI limits withdrawals to ₹50,000

In the Yes Bank crisis, one chart shows how rumours were used to trap small investors

Bad loans take the wind out of Yes Bank— swings to a loss in the second quarter

Yes Bank profits dropped 91%-- but it was still way better than expectations