Bajaj Auto shareholders will look for cost controls and CEO confidence as sales remain a lost cause due to the lockdown

Jul 21, 2020, 10:48 IST

- Bajaj saw a massive decline of 64% in the first quarterly sales volume.

- Bajaj rural sales have shown a positive recovery, driven by healthy Rabi procurement and strong progress of Kharif sowing.

- The credit rating agency, Moody’s earlier in May said it expects the global auto sales to fall 20% in 2020.

Advertisement

The lobby of Indian automakers called the last three months as the ‘worst quarter’ in over 2 decades and Bajaj Auto (the country's largest 3-wheeler maker and second largest two-wheeler maker) wasn’t immune to it either. Sales volumes were down 64% between April to June 2020 compared to the same time last year.According to various analysts reports, Bajaj is projected to see a profit dip of nearly 42%.

| Brokerage | Decline in net profit |

| Edelweiss Securities | -43% |

| Emkay Global | -44.30% |

When other companies clocked zero sales in the month of April, Bajaj was the only company to sell nearly 32,009 units, though it was down 91% year-on-year. However, as the market opened up in June, Hero managed to beat Bajaj in sheer volumes for the quarter.

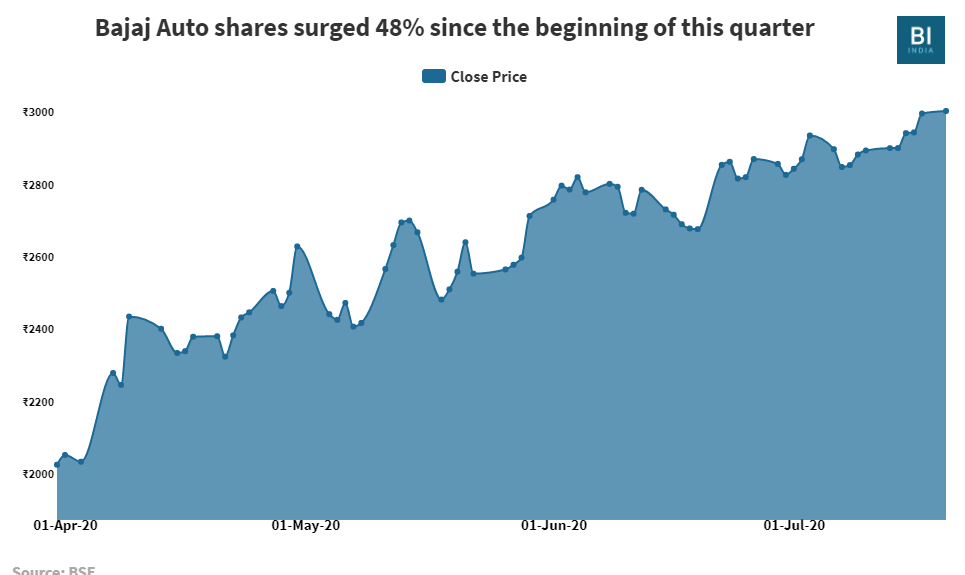

According to Brokerage firm Sharekhan, Bajaj rural sales have shown a positive recovery, driven by healthy Rabi procurement and strong progress of Kharif sowing. Semi-urban areas have also been witnessing a strong pick-up driven by an increased preference for personal transport to ensure social distancing. And, that is the reason the stock has run up 48% since March 31 until now, as investors are betting on the company's long-term prospects.

Advertisement

The outlook for the auto industry is pretty bleak as of now, not just in India but across the world. The credit rating agency, Moody’s earlier in May said it expects the global auto sales to fall 20% in 2020.

In its last post-earnings investor call, the management said it expects a “smart recovery” in the second half of the year. It has to be seen if CEO Rajiv Bajaj’s confidence is shaken by the pace of recovery so far.

| Brokerage | Reco | Target Price |

| Motilal Oswal | Neutral | ₹2895 |

| Sharekhan | Buy | ₹3250 |

| Axis Securities | Hold | ₹2637 |

SEE ALSO: Chai and sanitiser may save the quarter for Hindustan Unilever

Advertisement

Serum Institute of India to soon apply for local trials of AstraZeneca-Oxford Covid-19 vaccine