What is a bad bank and why are some people pushing for it ahead of Budget 2021?

Jan 19, 2021, 13:02 IST

- India’s upcoming budget may set out a framework for setting up a bad bank to handle the expected influx of bad loans post-pandemic.

- According to the Reserve Bank of India (RBI), gross non-performing assets (NPAs) could balloon to 14.8% by September under the worst-case scenario.

- A bad bank would allow regular banks to sell their bad loans and focus on bringing in new business.

Advertisement

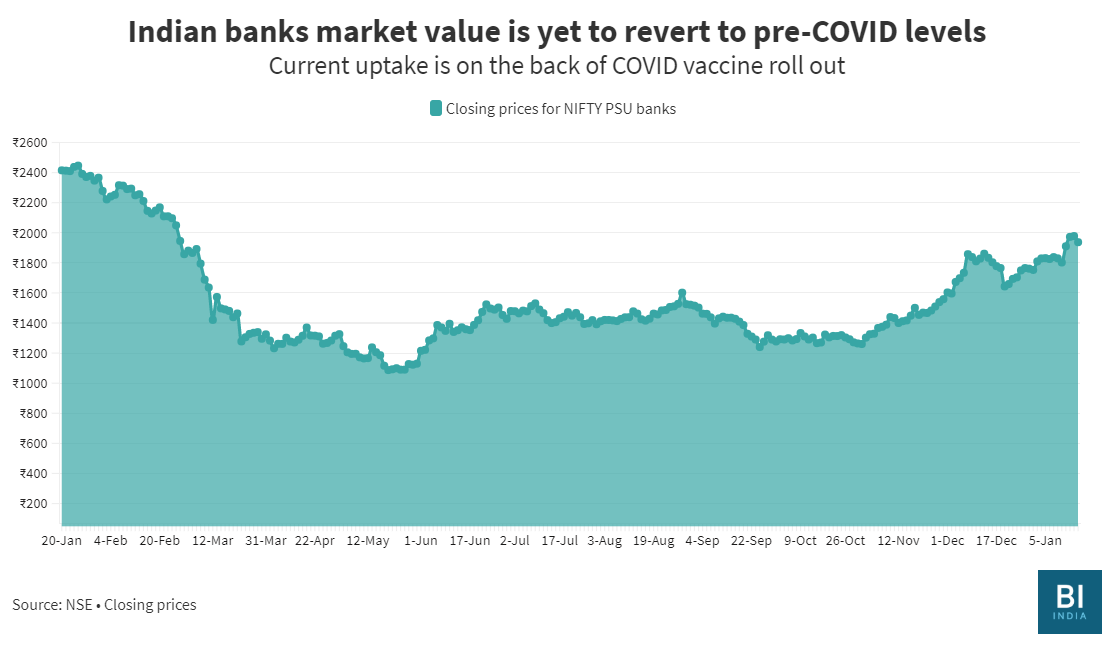

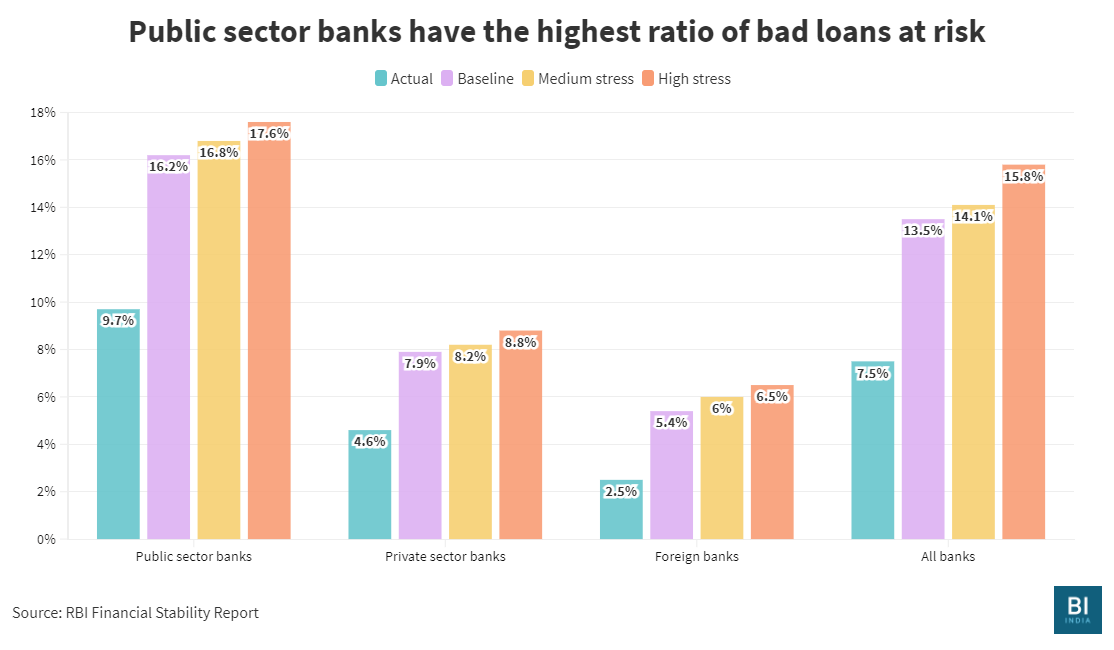

India’s government owned banks like State Bank of India, Punjab National Bank and Bank of Baroda have a huge amount of bad loans. Anywhere from 16.2% to 17.6% of all the money that these public sector banks have lent are unlikely to return or are under stress. This may only get worse and which is why the proposal for a bad bank, which will absorb all these sour loans, is back on the table ahead of the Union Budget 2021 scheduled on February 1.

Even the RBI Governor Shaktikanta Das recently indicated that the central bank is open to the idea of creating a bad bank. “If there’s a proposal to set up a bad bank, the RBI will look at it. We have regulatory guidelines for asset reconstruction companies,” Das said speaking at an event on January 16.

What is a bad bank?

If a bad bank is set up in the upcoming budget, it will have the power to purchase bad loans from banks at the market price. It acts as an aggregator of all the stressed assets in the banking system.

Advertisement

The Finance Ministry has reportedly reached out to stakeholders for inputs on the likely framework.

RBI itself is fearing that the amount of loans that may go bad is likely to rise

Indian banks are on the cusp of a fresh cycle of bad loans, and a setting up of a bad bank may be on the docket for Nirmala Sitharma’s ‘never-seen-before’ 2021 Budget. The Reserve Bank of India (RBI) has projected that bad loans may hit 14.8% by September under the worst-case scenario — nearly double from the current 8.5%.

Advertisement

The government is mulling the proposal of creating a bad bank to avoid excessive dependence on capital infusion. Thanks to the series of measures announced by the government as part of its ₹20 lakh crore stimulus package, and liquidity measures from the RBI through the pandemic, the banking system is flooded with excess liquidity right now.However, that may no longer be the case as the business environment gets tougher, while the demand for credit continues to stagnate, and bad loans continue to increase.

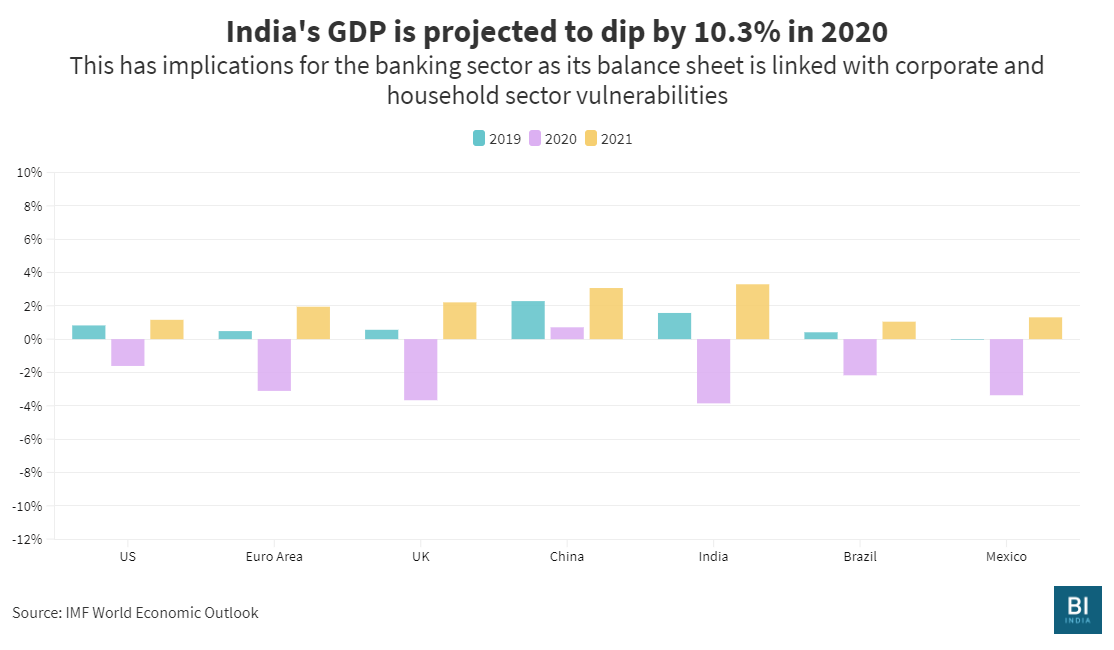

This has implications for the banking sector as its balance sheet is linked with corporate and household sector vulnerabilities

"We are looking at various options, including the option you mentioned [of a bad bank], and it is still in the works... The RBI has been asking us, and we ourselves also feel that we need to recapitalise. We have recapitalised to a large extent and this year too, we have kept some money for recapitalisation so that commitment is there," the Department of Economic Affairs (DEA) Secretary Tarun Bajaj told the Confederation of Indian Industries (CII) in December.

| Bank group | Liquidity coverage ratio as of 30 September 2020 |

| Public sector banks | 181.83% |

| Private sector banks | 148.35% |

| Foreign banks | 201.32% |

Advertisement

One bad bank or many

While the privatisation of banks — or at least the reduction of government stake in public banks — is currently on the cards as well, experts believe that an Indian bad bank should be spearheaded by the government until there’s a change in the status quo.

Meanwhile, the industry body CII, has recommended that the government create multiple bad banks by allowing Alternate Investment Funds (AIFs) to buy bad loans.

"Hitherto the NPAs have largely been sold to asset Reconstruction Companies (ARCs) only and mostly not for cash consideration which means that the sale price was not a ‘true sale’ since ARCs could pay through 'security receipts',” explained the Pre-Budget Memorandum 2021-22.

Security receipts are an instrument where the payment is made only upon recovery of some money — a sort of participatory note. According to the RBI, outstanding security receipts currently stand at around ₹1.46 lakh crore and recovery is a mere 10-12%. Without recovery, there isn’t any cash going back to the banks.

Advertisement

"The need of the hour is to increase avenues for ‘cash realisation’ against sale of loans and to increase avenues for capital to compete for such loans to maximize realisation for banks,” said the apex industry body. It proposes allowing AIFs and foreign portfolio investors (FPIs) to purchase bad loans and make the market more competitive with the asset reconstruction companies (ARCs).Bad loans during COVID-19 and its aftermath

The stock market may have recovered but the true impact of COVID-19 on businesses is yet to emerge.

For now, the onslaught of non-performing assets (NPAs) has been kept at bay due to the RBI’s loan moratorium, which was in place till 31 August 2020.

The Supreme Court further put a stay in place to hear petitions requesting the extension of moratorium, compound interest accrued, possible restructuring and other matters with respect to issue. The apex court is yet to announce its verdict.

Advertisement

The timing seems right for the Finance Ministry to consider the creation of a ‘bad bank’ with the Indian banking system gearing up to deal with a spike in bad loans and assess the true extent of stressed assets post the pandemic.

Sitharaman has a tall order to fill when it comes to banking reforms during this year’s budget with privatisation of banks and creating demand for credit also on the docket.

SEE ALSO:

Indian government’s budget dilemma – curb the sale of cigarettes or let the over $12 billion tobacco industry provide the much needed cash