Ever since

Ever since To encourage affordable housing in urban locations, National Housing Bank(NHB) has come up with a refinance scheme, wherein

This is a great initiative. A 'fixed home loan' for small loan borrowers, who do not plan to repay their loans in next 10 years, seems apt.

However, to make the most of this scheme, borrowers first need to understand what it is all about to decide on a property purchase and subsequent home loan borrowing. To make things slightly easier for them, we have jotted down a few important points. Read on…

Property you can buy includes

You can avail the scheme for purchasing a readily-constructed or under-construction home. It can also be used for purposes like home extension or home improvement of the dwelling unit. For example, if you already own a single-storey house and you want to construct the first floor, you can opt for home loan under this scheme. Or, if you want to increase another room in your existing home, loan can be given to you in this scheme too.

Please note that plot loans are not covered under this scheme as the essence is all about 'a roof over the head'.

Scheme commences on

This is applicable to all home loan borrowers w.e.f. 16th March 2015. The borrower needs to apply to the HFC, mentioning this scheme requirement clearly at the time of application.

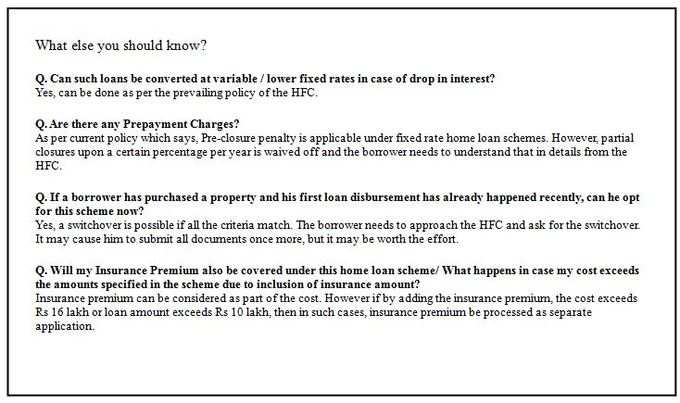

Terms & conditions for the loan

Fixed rate of interest is offered for initial 10 years and variable thereafter. Variable rate can be offered only if the customer opts for more than 10-year term, of which initial 10 years will be locked at fixed rate. If the customer wants only fixed rate, then the maximum term can not exceed 10 years.

Simple variable Home Loan products can’t be offered under this scheme.

Rate of interest that you would pay

The following rate is applicable for both salaried & self employed borrowers:

9.85% p.a. fixed rate for initial 10 years & variable thereafter linked to HFC's Prime lending Rate(PLR). The spread from PLR will be fixed on the date of disbursement and announced in advance by the HFC.

For example, if the current PLR is 17% and the spread offered is 7.15%, then upon completion of the first 10 years' fixed term, if the then applicable PLR is 18%, the applicable variable rate for the borrower will be 18%-7.15%=10.85% p.a.

Miscellaneous

· Under this scheme, you are entitled for a 20-year loan term, unlike some other popular 30-year term, lenders do offer in the market.

· You can buy property only in urban areas(as per 2011 census) under this scheme.

· The maximum loan amount you get is Rs.10,00,000/- (Ten lakhs).

· Processing fee is applicable as per HFC's policy.

· Property cost or area measurement- either of the following should not exceed

o Cost should not exceed Rs.16 lakhs OR

o Carpet area should not exceed 60 sq.mt. i.e. 645 sq. ft. approximately.

· Only people with family income less than Rs 4,00,000/-(Four lakhs) per annum can avail this benefit.

This scheme should bring smile for the section who felt deprived of any special facilities for a very long time from the

HFC-s. The priority sector lending had lost the sheen as anyone who was borrowing lesser amount was getting the leverage. There was no specified income group or property size or price wasn't looked at very seriously.

People should get encouraged to buy their own homes and enjoy the fixed rate stability for the next 10 years and relax. #AccheDin.

(About the author: This article has been contributed by Sukanya Kumar, Founder and Director of RetailLending.com.)