Year 2015 was quite a mixed bag for the Indian economy. Growth expectations soared as the new government started introducing strong policy measures aimed at improving the ease of doing business in India.

Year 2015 was quite a mixed bag for the Indian economy. Growth expectations soared as the new government started introducing strong policy measures aimed at improving the ease of doing business in India.This accompanied with RBI’s focus on inflation control and foreign direct investments brought world attention back to the India growth story.

The year also saw specific measures being taken by the government for different sectors to augment growth including renewed focus on manufacturing with the launch of ‘Make in India’ campaign.

The year witnessed, what we call, hyper-growth in the technology start-up and software product landscape with India ranking as the fourth largest start-up hub in the world with over 3,100 start-ups in the country.

So what does all this mean from Executive Compensation perspective?

The projected fixed pay for top management has gone down from 9.7% to 9.5%. A substantial part of compensation today for a CEO is not guaranteed in nature and is aligned to short term or long term goals in some way, this essentially means putting performance first.

These plans get impacted by host of factors like nature of industry, business life cycle stage of the company, specific performance objectives that the company wants to drive etc. More and more companies that have traditionally used LTI instruments with low performance alignment are looking at changing the plan structures to bring in greater performance orientation.

Having said that, the word of caution from our standpoint is that – while it is right to have performance orientation, due care should be given to ensure that there is no excessive risk taking by the executives that may prove to be counterintuitive for the company in long run.

This excessive risk taking can be mitigated by having the right set of risk adjusted performance metrics in your plans. Deferrals, Co-investment plans, Clawback and malus provisions are other simpler ways of doing this.

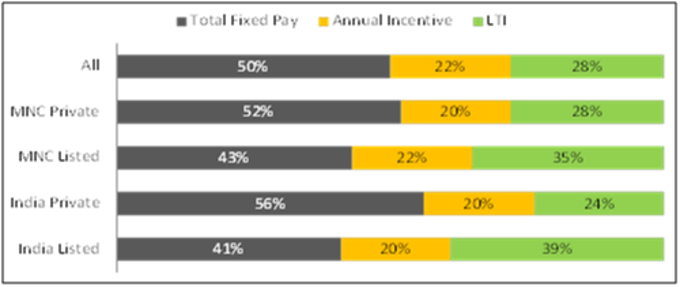

Aon Analysis of compensation structure for CEOs in organizations that offer both short and long term incentives as part of the pay structure show a 50-50 ratio of fixed and variable compensation (variable compensation includes both short and long term incentives). This ratio, over the years has moved in favour of variable pay over the years.

Indian listed companies are most aggressive when it comes to “pay at risk” with approximately 41% of total compensation attributed to fixed pay and balance 59% to short and long term incentives.

In our view, it makes a lot of sense for organizations to have considerable amount linked to stock based plans. These plans not only link a considerable part of top management compensation with stockholders’ returns and fundamental performance of the company but also have an advantage for listed companies as upside gets funded by the market.

As the compensation programs mature, a higher proportion of compensation will get attributed to long term incentives although it might take some time for Indian companies to reach the proportions we see in the western markets like the US.

Higher attribution to long term incentives will also lead to rationalization of long term incentive programs by companies. What we see happening in India has an uncanny resemblance to what we saw happened in the US years ago. As the prevalence and quantum of long term incentives goes up, these programs may undergo a structural change.

With the change in accounting norms under IND-AS, increase in volatility and high dilution levels, we can expect prevalence of instruments like Performance Shares to go up in coming years.

These programs are less dilutive in nature compared to

(This article is authored by Anubhav Gupta, Solution Head, Executive Compensation and Governance, Aon Hewitt India)

(Image: Thinkstock)