Energy for all is the need of the hour, especially in an emerging

economy like

India where a big chunk of the population still can’t access

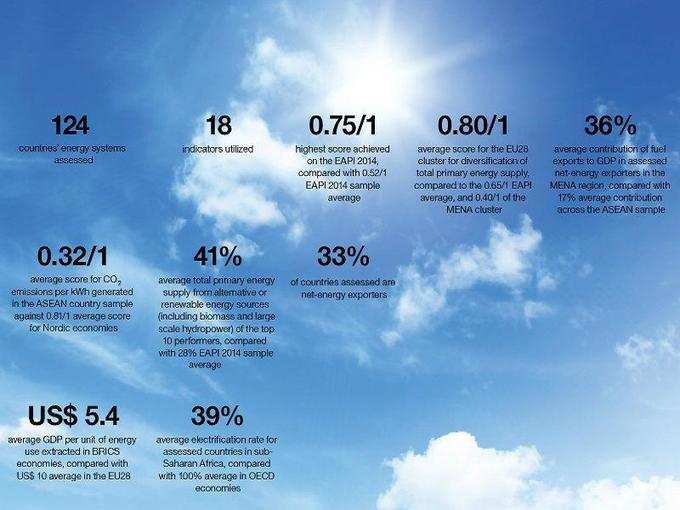

modern energy sources and the overall growth of the country suffers due to such non-inclusion. The outlook is not exactly bright at this point as India ranks 69th among 124

countries in the recently released

Global Energy Architecture Performance Index (

EAPI) Report 2014, prepared by the

World Economic Forum in collaboration with

Accenture.

India, with an overall score of 0.48, has the second lowest

energy performance in the

BRICS cluster that also includes

Brazil,

Russia,

China and

South Africa. Interestingly, China lies at the bottom among the

BRICS (85th with a score of 0.45), but other countries in this group are way ahead of India and its neighbour. Ranked 22nd, Brazil tops the BRICS group with a score of 0.64, extracting 50% more

GDP per unit of energy use than the average of the other

BRICS countries. It is followed by the Russian Federation (28th, with a score of 0.62) and South

Africa (54th, with a score of 0.54).

The top 10 performers are mostly EU and/or

OECD nations –

Norway,

New Zealand,

France,

Sweden,

Switzerland,

Denmark,

Spain and

Latvia – with the exception of

Colombia (7th) and

Costa Rica (9th). The US came in 37th, followed by

Japan. The regions covered in the report include

EU28,

MENA, BRICS,

North America,

Sub-Saharan Africa and the

ASEAN.

Why we need EAPI Before we consider why India is lagging behind the rest, it is important to understand the dimensions of the ‘

energy triangle’ and what it takes to achieve top-level energy performance. During the past three years, the World Economic Forum has been working on the

new energy architecture, defined as the integrated physical system of

energy sources, carriers and demand sectors. The ‘energy triangle’ frames the key objectives of the

energy architecture – the ability to provide secure, affordable and

environmentally sustainable energy supply. Accordingly, the Global Index has used 18 indicators to assess 6 regions and 124 countries under three baskets –

economic growth and development,

environmental sustainability and

energy access & security – while analysing the complex trade-offs and dependencies that affect the efforts of each country under review.

“Resource, wealth or

economic development alone do not guarantee high performance on the Index,” said Roberto Bocca, senior director and head of energy industries at the World Economic Forum. “For an

effective energy system, countries need to focus on all three sides of the energy triangle – environmental sustainability, security of supply and affordability,” he added. Undoubtedly a difficult task, if you look at the toppers or any other country, for that matter. No single country has got a top score of 1/1 for the overall Index (an average of the scores posted under the three heads) and no one has hit a ‘perfect 1’ either, under any of the three baskets.

Four factors hindering India’s energy performance

Low access:

Four factors hindering India’s energy performance

Low access: Let’s look at the grassroots first. Energy access across BRICS is high, with the exception of India and South Africa which continue to face

lower electrification rates for rural and low-income groups. In fact, India is the lowest performer within the BRICS cluster (0.54/1), with only 75% accessing modern energy sources. It means around 293 million people go without those, compared to just 4 million in China.

However, there are longer-term solutions on the cards. Alongside a number of national and international initiatives, the government is currently running the Restructured Accelerated Power Development and Reform Programme or

R-APDRP, directing around $10 billion over the coming years for

grid modernisation. India has also launched a

Remote Village Electrification programme while the

Ministry of New and Renewable Energy is targeting the installed capacity from new

renewables to reach 21,700 MW by 2017 (more on India’s

green power here).

Increasing reliance on energy imports: Large-scale economic expansion across the country has triggered bigger

energy consumption and a crippling dependence on imports – a major factor behind the ballooning trade and

current account deficits. India is one of the biggest importers of crude oil and more than half of its $191 billion

trade deficit in FY2013 – $109 billion, to be precise – accounted for oil, with the country importing around 82% of its requirements, mostly from the

Gulf countries. Overall, 28% of the country’s

net energy consumption is met through imports and among the BRICS, India has the

highest spend on fuel imports relative to GDP (10%).

It’s a kind of vicious cycle, to say the least, which is negatively impacting the

Indian economy. “The whole mess in the

CAD is due to the imports of both coal and oil,” Vivek Pandit, senior director for energy at the Federation of Indian Chambers of Commerce and Industry (

FICCI) told

FT. Worried by the current account deficit,

FDI and

institutional investors gradually started withdrawing their support since March this year. This fuelled a substantial weakening of the

Rupee and resulted in a drawdown of

foreign exchange to the tune of $12.8 billion. According to a PwC report, the drawdown could have been avoided, had India produced 17 million tonnes more oil than its current domestic production.

Worse still,

India’s oil import dependency is forecast to grow another 10 percentage points to exceed 90% by 2031. While increasing domestic exploration will help to a certain extent, India must try and curb the

oil bills further by seeking new suppliers and buying more stake into African and other

non-Gulf oil and gas assets.

This part of the strategy is slowly taking shape as

ONGC Videsh, the overseas investment arm of

India government’s flagship oil and gas explorer

Oil & Natural Gas Corp, has been pushing hard to build up a

diversified portfolio of foreign assets to minimise the country’s dependency on the Middle East.

ONGC Videsh has recently signed two multi-billion-dollar deals to buy into offshore natural gas assets in

Mozambique. It has a significant presence in

Latin America and is also looking for exploration assets in

Myanmar,

Bangladesh,

Lebanon and

Australia.

Prevalence of energy subsidies: Another factor that is dragging India down by increasing oil demand and widening the budget deficit. Both India and Russia are the lowest performers for the indicator on

liquid fuel subsidies. India’s subsidies for diesel put it in the lower quartile globally for this indicator even as the country is trying to improve

energy affordability and access for lower-income groups.

Coal-dependence hurts: At present, coal dominates the country’s

energy mix with a robust 53% share in

primary energy consumption, affecting India’s score in terms of environmental sustainability. The country has scored 0.41/1, underlining the challenge it faces in diversifying the energy mix beyond

fossil fuels. Although energy trade can have positive impacts here, it can also pose economic and

energy security risks, especially as we are dependent only on a few trading partners.

Interestingly, 41% of the

energy supply in the top 10 countries comes from low-carbon energy sources, compared to a global average of 28%. India, too, is rolling out low-carbon power generation through plans to increase

nuclear capacity from the current 4.4 GW to 5.3 GW by 2016.

The bottom line “Our analysis concludes that there is no single way forward; each country must work with its own resources and constraints, making difficult choices and trade-offs,” said Arthur Hanna, Managing Director, Energy Industry, Accenture, and a Member of the World Economic Forum’s Global Agenda Council on New Energy Architecture. “The Index helps nations take stock of their energy transition challenges and address key barriers to success, such as market distorting subsidies, continued uncertainty around energy policy and funding for research and development of

new energy sources and technologies.”

Keeping that in mind, can India cope with the transition and morph its energy policies accordingly?

Top Image: Wikipedia

Data chart: World Economic Forum